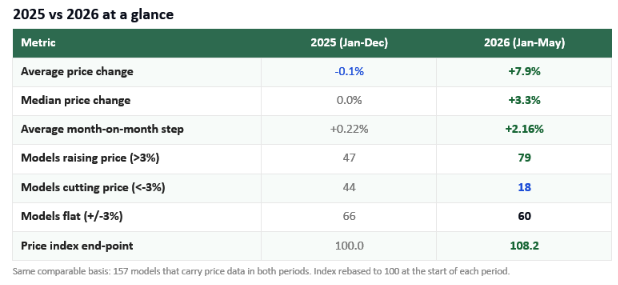

India’s smartphone market split into two distinct pricing eras within eighteen months. Through calendar 2025, prices went nowhere; the Techarc price index fell to a trough of 94.9 in September before recovering to exactly 100 by December, leaving the average phone essentially flat (-0.1%) for the year. Then, from January 2026, prices broke sharply upward. In the first five months of 2026 alone, the average launched-in-2025 model rose +7.9%, with the index climbing from 100 to 108.2 by May.

The driver is a memory-cost shock passing through to retail. Its incidence is strikingly regressive: budget tiers absorbed the increase while premium tiers continued to discount. This report compares the two periods across the industry, segments, brands, and models, and sets out what it means for the second half of 2026.

Key takeaways

- 2025 was a year of discounting and stabilisation; 2026 is a year of broad-based price increases. The reversal is not subtle; increases outnumbered cuts roughly 1-to-1 in 2025, but 4.4-to-1 in 2026.

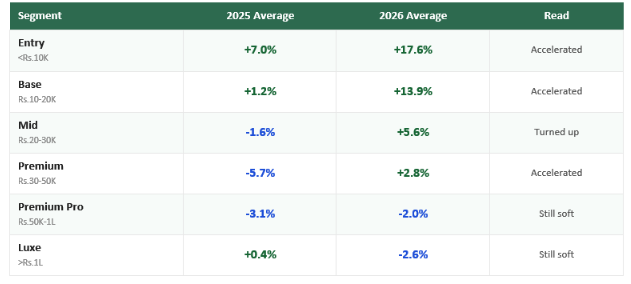

- The shock is regressive. In 2026, the Entry tier (< Rs. 10K) rose +17.6% and Base (Rs. 10-20K) +13.9%, while Premium Pro and Luxe still fell. Cheaper phones, where memory is a larger share of the bill of materials, took the hit.

- The Mid segment flipped. Rs. 20-30K phones fell -1.6% in 2025 but rose +5.6% in 2026 – the clearest sign the increase is broadening up the price ladder.

- Premium discounting persists. Premium Pro (Rs. 50K-1L) and Luxe (>Rs. 1L) declined in both periods, as brands protected volume at the high end even while raising entry prices.

- Budget-focused brands led the increases. Acer, Ai+, Redmi, CMF, Infinix, and Poco posted the steepest 2026 gains; Xiaomi, Itel, and Alcatel were the notable price-cutters.

- The momentum is intact through May 2026. The index rose every month of 2026 so far (100.0 to 108.2), with no sign yet of the increases reversing.

Industry Pricing Trend

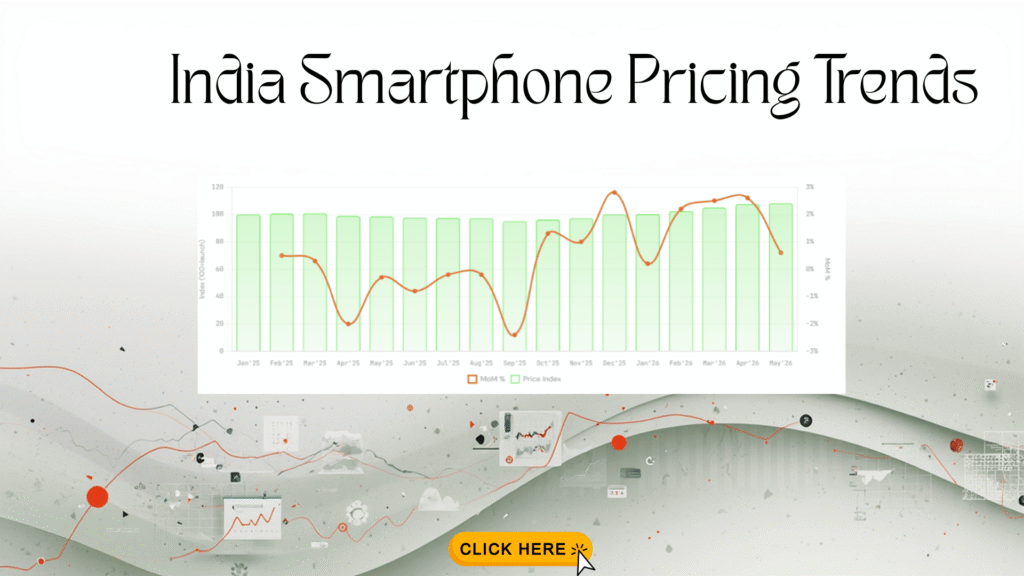

2025: a V-curve that went nowhere

Across 2025, the average launched-in-2025 smartphone traced a shallow V. Prices held near launch through Q1, drifted down through mid-year as launch-season premiums unwound, and bottomed at 94.9 in September, roughly 5% below launch. A year-end recovery then pulled the index back to 100.0 by December. Net movement for the calendar year was essentially nil (-0.1% average, 0.0% median). With 47 models rising, 44 falling, and 66 flat, 2025 was a market in balance – the familiar pattern of post-launch discounting offset by festive-season firmness.

2026: a clean break upward

2026 broke the pattern. From a January base of 100, the index rose in every subsequent month – 102.3, 104.7, 107.7, and 108.2 by May – an average gain of +7.9% in just five months and a month-on-month step (+2.16%) nearly ten times the 2025 pace (+0.22%). Seventy-nine models raised prices against just eighteen cuts. This is no longer post-launch noise; it is a coordinated, market-wide repricing as component-cost inflation – memory in particular – reaches retail shelves.

The contrast matters for interpretation. A buyer who waited through 2025 was rewarded with stable-to-falling prices. A buyer waiting through 2026 has been penalised. The discount era that conditioned Indian smartphone buyers to expect prices to fall after launch has, for now, ended.

Segment Analysis

The Techarc six-tier framework shows where the increase landed, and where it did not.

The regressive gradient is unmistakable. In 2026, the price increase is steepest at the bottom (Entry +17.6%) and fades monotonically up the ladder until it turns negative above Rs. 50K. Every tier from Entry through Premium moved up versus 2025; the two highest tiers continued to ease. The economics are straightforward – in a sub-Rs. 15K phone, a memory price increase is a large share of the bill of materials and cannot be absorbed, whereas a Rs. 80K flagship has the gross margin to hold or cut its price to defend share.

The Mid-segment swing (-1.6% to +5.6%) is the bellwether. It signals the increase is migrating upward through the price ladder, not staying confined to budget devices – the single most important trend to watch into H2 2026

Brand Analysis

Who raised, who cut: In 2025, most brands clustered near flat. The few movers were budget-led: Acer (+18.2%, single model), Infinix (+12.2%), and iQOO (+6.4%) on the upside; Nothing (-10.0%), Google (-5.1%), and Honor (-3.8%) on the downside. In 2026, the dispersion widened sharply and tilted upward.

The pattern is consistent with the segment story. The brands raising prices most are concentrated in budget and value tiers (Acer, Ai+, Redmi, CMF, Infinix, Poco), where the cost pressure is most acute and least absorbable. The price-cutters are either premium-positioned (Xiaomi’s high-end, Apple holding flat) or fighting for share at the bottom (Itel, Alcatel). Apple’s flat reading across five models is itself notable – pricing power and ecosystem lock-in insulate it from the component-cost cycle that is reshaping the rest of the market.

A caution on single-model brands. Acer’s +63.7% reflects one device and should be read as an outlier signal, not a portfolio strategy. The most reliable brand reads come from those with several models in-market – Infinix, Poco, Redmi, Realme, Samsung, and Vivo.

Model-Level Movers

At the model level, the two periods look entirely different. In 2025, even the biggest risers topped out around +20% (Lava Shark 5G, Infinix Note 50s 5G, iQOO Z10 Lite 5G, Vivo T4 Lite 5G – all +19% to +21%), and steep cuts were common (Realme GT 7T -25.6%, Samsung Galaxy A06 -20.8%). The distribution was wide and roughly symmetric.

In 2026, the top of the distribution stretched far higher, and the bottom compressed. The Acer Super ZX 5G (+63.7%), Infinix Smart 10 5G (+50.0%), Infinix Hot 60i 5G (+45.5%), and Samsung Galaxy M06 (+40.9%) all posted gains no 2025 model approached. Declines became rarer and shallower, led by Xiaomi 15 Ultra (-18.2%) and Realme 15 Pro 5G (-17.2%) at the premium end. The asymmetry – many large increases, few cuts – is the model-level fingerprint of cost-push inflation.

Techarc View: Outlook to H2 2026

- The increases will prove sticky. Prices that buyers have already accepted in the Rs.8K-Rs.18K band are unlikely to be voluntarily rolled back, even if memory costs ease. Expect the 2026 step-up to hold rather than reverse.

- Watch the Mid segment. The Rs. 20-30K swing from -1.6% to +5.6% is the leading indicator. If it continues to firm in H2, the increase has successfully migrated up-market and will be harder to dislodge.

- Premium remains a discounting battleground. With Premium Pro and Luxe still negative, expect continued promotional intensity at the top as brands trade margin for flagship volume – the opposite of their budget-tier behaviour.

- Budget-brand pricing power is the story to track. Acer, Ai+, Redmi, CMF, Infinix, and Poco are testing how much budget buyers will absorb. Their H2 pricing will reveal whether this is a durable repricing or a temporary cost pass-through.

Methodology. Based on monthly retail price tracking of 165 smartphone models launched in India in calendar year 2025, across 22 brands, from January 2025 to May 2026. Launch is the first month a price is registered. The 2025 view measures movement Jan-Dec 2025; the 2026 view measures Jan-May 2026; each is rebased to 100 at period start. Two clear data-entry outliers were corrected to the model median. Models without at least two price points in a period are excluded. Segments follow the Techarc six-tier framework.