In the past decade the rapid growth of fibre connectivity coupled with the recent 5G (five-G) deployment has resulted in a reliable broadband internet alternative to enterprises across domains of banking, industries, government, defence, education, etc. This has started reflecting on the prospects of technologies like V-SAT, once considered to be the backbone of high-speed reliable internet connectivity in enterprise domains especially in banking to connect branches and ATMs, industries like offshore refineries, defence establishments, educational institutions, etc.

Today with ‘carpet coverage’ of 5G and fibre, enterprises and institutions are fast relying on cellular and fibre high speed broadband as their primary internet connectivity resulting in decline in V-SAT appetite. India’s 5G coverage spans 99.6% of districts which serves 80% of the population. Similarly, telecom operators, especially Jio has led to an unprecedented last mile fibre connectivity across India including tier 2 & 3 cities and towns. While this is already showing its results on the home user segments, the enterprise connectivity is also up for transformation with businesses relying on these mediums as their primary source of internet connectivity.

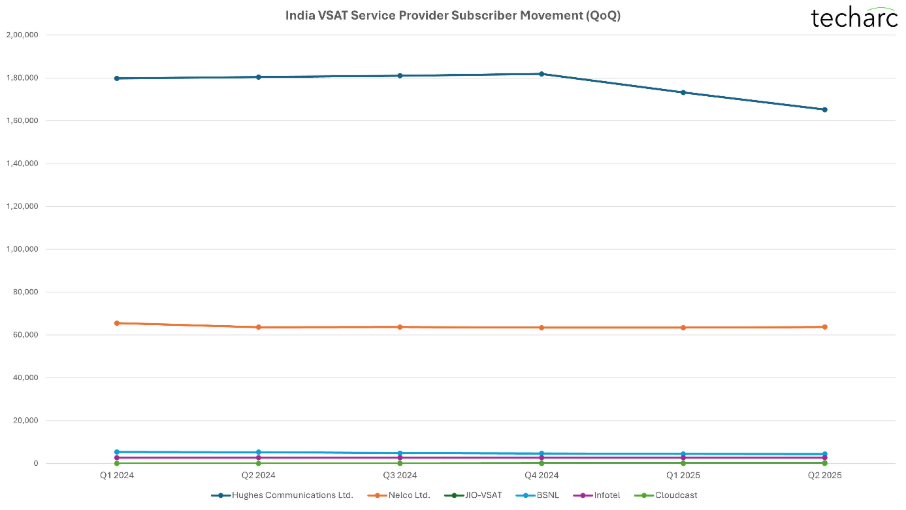

Excluding remote and difficult terrain areas, even in sectors like banking, V-SAT connectivity is becoming secondary (redundant) medium of connectivity. Beginning 2025, there has been a sharp dip witnessed in V-SAT subscribers in the country, with three incumbent service providers – Hughes, Nelco and BSNL all started losing its customers. Together these three service providers capture over 98% of the market share of V-SAT services in India. The other two operators – cloudcast has been statically serving 7 customers and Infotel has also seen a minor dip in its subscriber numbers. The only operator which has been able to gain customers is Jio, which in less than a year has added 129 customers for V-SAT. It needs to be seen if Jio can pull further from here and cause a major stir in this segment too like it has done in other segments. That would mean displacing Nelco and Hughes, primarily Hughes which leads this market with a huge gap!

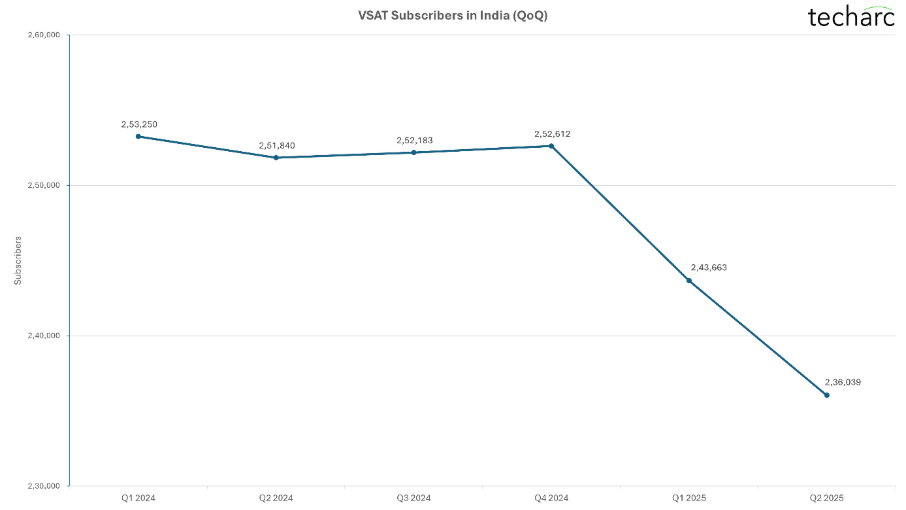

In 2024, while the V-SAT subscribers in India leveled around 2.5 Lakh, by the mid of 2025, it has dipped to 2.36 Lakh, reflecting a decline of ~6% in a short period of just 6 months!

The enterprises are getting better internet speeds, lower latency and cost-effective internet services from other mediums like fibre and cellular (5G), along with availability and coverage across any location. The service reliability and quality have also significantly evolved over the period to that of an enterprise grade. This is resulting in the substitution of medium and both F (fibre) & F (5G) are gaining in enterprises making the prospects of VSAT, undoubtedly ‘very small’.

Key Insights of the V-SAT Market

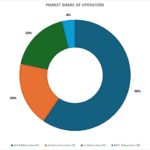

- Hughes Communications, despite declines with -8,674 in Q1 and -7,985 in Q2, leads the market as of Q2 2025 with a 69.97% market share, followed by Nelco at 26.98%. Jio-VSAT accounted for 0.05%, while BSNL held 1.14%. Cloudcast reported 0% share, as its subscriber base remained unchanged at 7 users throughout 2024 and 2025.

- Market down -6.6% in H1 (Q1 & Q2) 2025; total base stands at 236,039.

- 2024 saw low single-digit quarterly growth at the market level, turning slightly positive in Q4 2024 (+0.17%), but momentum reversed sharply in Q1 2025 (-3.54%), then remained negative in Q2 2025 (-3.13%).

- Nelco is the relative gainer in 2025 with expanding share and net adds, positioning it as the primary beneficiary of customer migrations or new demand pockets. Gained share to 26.98% with +345 net adds in Q2 2025

- Jio-VSAT’s re-entry adds a competitive vector; though tiny, consistent net adds signal a gradual footprint build in specific segments.

- BSNL’s stabilization could reduce share loss drag on public-sector accounts, but material recovery is not yet visible. Their losses moderated to -11 in Q2 2025

The main dip comes in the customer base of Hughes, pulling down the overall V-SAT market. Hughes has been servicing all leading industry segments with its V-SAT solutions. These include banking, oil & gas, defence and government. The dip could be a reflection of reducing scope of V-SAT services across these sectors, especially banking which is moving towards hybrid connectivity where cellular / fibre mediums are front-ending increasingly. Looking at the subscriber movement of the V-SAT service providers, the loss of Hughes customers has not been gained by any other operator indicating that these enterprise customers have opted for substitutes of V-SAT connectivity.

The market still is in command of Hughes with 70% of the share by subscribers, distantly followed by Nelco with another 27%. The remaining of the operators are insignificant and also showing a declining trend in numbers, except Jio which is the newest V-SAT operator. Considering how Jio has operated in other segments it’s highly likely that the market shares in this category will also go for a big change in coming quarters, where despite the V-SAT subscribers continuing to decline, Jio will look for increasing the market share aiming to be the leader here as well.

It’s too early to call it ‘full n final’ settlement of V-SAT connectivity in India. With the SatComm due for new orientation after Starlink appearing on the scene and certain areas and regions in India continuing to be extremely difficult to be connected through cellular or fibre, the role of satellite connectivity cannot be nullified. It will remain an important connectivity medium to achieve of true 100% connectivity across the country. Even with this small number of deployments ranging 2.3 to 2.5 Lakh subscribers, it would translate in millions of end users benefiting from V-SAT connectivity through which they will continue to be part of financial inclusion, G2C services, and other benefits of internet.