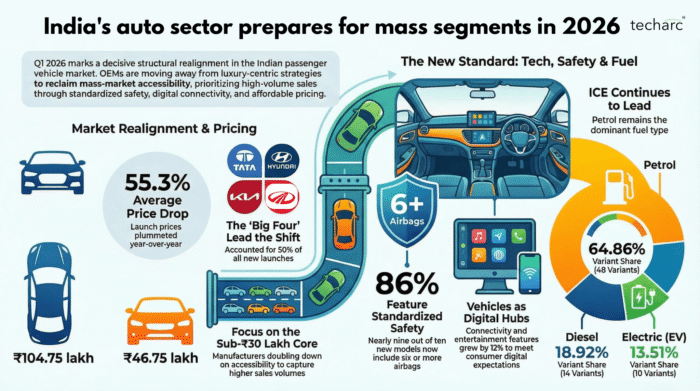

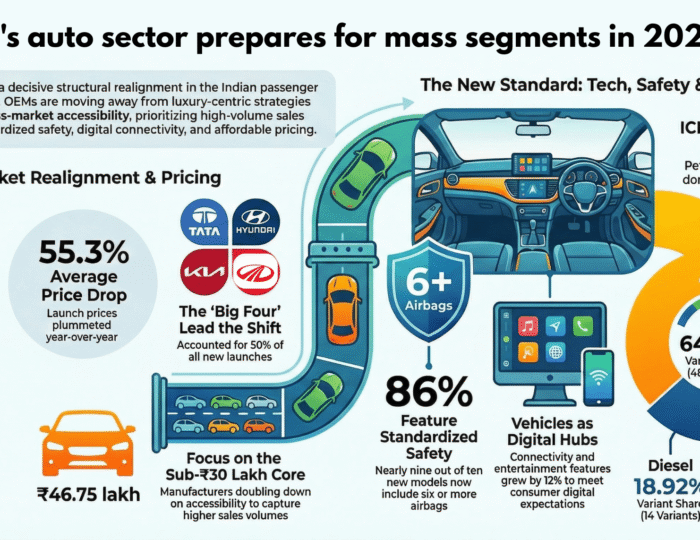

The first quarter of 2026 signals a decisive structural realignment within the Indian passenger vehicle sector, as the OEMs shift away from the premium-heavy strategies of the previous year to reclaim mass-market accessibility. While overall launch activity expanded, with 39 new models introduced by 19 OEMs, the average launch price experienced a contraction of over 55%, falling to ₹46.75 lakh. This shift reflects a strategic movement toward volume-driven growth, spearheaded by a concentrated group of core manufacturers who are aggressively integrating advanced safety standards and high-fidelity digital connectivity into more affordable, high-demand segments.

Key Takeaways

- Average Price Correction: The average launch price plummeted by 55.3% year-over-year, dropping from ₹104.75 lakh in Q1 2025 to ₹46.75 lakh in Q1 2026.

- The Big Four Leaders: Just four OEMs, Tata, Hyundai, Kia, and Mahindra, accounted for 50% of all new model launches this quarter, focusing their competitive efforts on the sub-₹30 lakh core market.

- ICE Still Leads: Petrol engines continue to drive the majority of new releases (nearly 65%), while Electric Vehicles (EVs) maintain a steady but lukewarm foothold at 13.5% (10) of launches.

- Safety as Standard: A significant shift in consumer protection sees over 86% of new models featuring six or more airbags as standard, with 50% offering ADAS Level 2.

1. Macro Market Shift: Prioritizing Accessibility

Q1 2026 illustrates a structural change where market activity broadened even as prices cooled. The number of OEMs rose from 17 to 19, and total model launches increased from 37 to 39.

The sharp 55.3% decrease in average launch price indicates that OEMs are abandoning the 2025 philosophy that consumers only prefer expensive luxury vehicles. Instead, manufacturers are doubling down on accessible, lower-priced vehicles to capture higher sales volumes.

2. OEM Activity Concentration: The Competitive Core

Market momentum is highly concentrated, with four primary players driving half of the industry’s new launches:

Top Contributors: Tata, Hyundai, and Kia each executed 5 launches, while Mahindra followed with 4 launches.

Total Concentration: These 19 models represent almost 50% of the total 39 new models introduced this quarter.

Fragmented Long-tail: The remaining 50% of launches are distributed across 15 different OEMs, with many luxury and niche players (like Mercedes-Benz, Audi, and Renault) executing only single-model releases.

3. Feature Evolution: Safety, Security, and Digital Hubs

OEMs are aggressively enhancing feature sets to meet rising consumer expectations for digital integration and protection.

- Safety and Security: Safety features saw an 11% increase across 2025-2026 launches:

- ADAS Level 2: Approximately 50% of new launches now include semi-automated features like lane-keeping and adaptive cruise control.

- Airbag Proliferation: Over 90% of new cars now feature above six airbags, reflecting a universal shift toward higher safety benchmarks.

Entertainment and Connectivity

- Vehicles are evolving into mobile digital hubs, with these features growing by nearly 12% year-over-year:

- High-level connectivity is being prioritized to keep consumers integrated with their digital ecosystems in transit.

- Premium, high-fidelity entertainment is becoming a key competitive differentiator for mass-market OEMs.

4. Powertrain and Fuel Strategy

An analysis of the 74 introduced variants reveals a balanced but cautious transition to new energy:

4.1 Fuel Type, Variant Share

- Petrol, 64.86%: Remains the baseline for 48 out of 74 variant launches.

- Diesel, 18.92%: Maintains around 19% with 14 launches, utilized heavily by Mahindra, Tata, and Kia.

- EV, 13.51%: Represents 10 variants; shows programmatic integration into OEM portfolios.

- CNG, 2.70%: Limited to highly specific use cases with only 2 variants.

5. Market Outlook: Q2 2026 and Beyond

- Moving into the second quarter of 2026, the industry is expected to maintain its trajectory toward volume-driven, accessible segments.

- Manufacturers will sustain their focus on the sub-₹100 lakh bracket, prioritizing market penetration over low-volume luxury releases.

- The rollout of EV variants will continue on a parallel track with traditional Internal Combustion Engine (ICE) models rather than causing an abrupt market disruption.

- Expect fierce rivalry among core manufacturers as they solidify their footing in the mass-market space, leveraging safety and connectivity as their primary sales drivers.