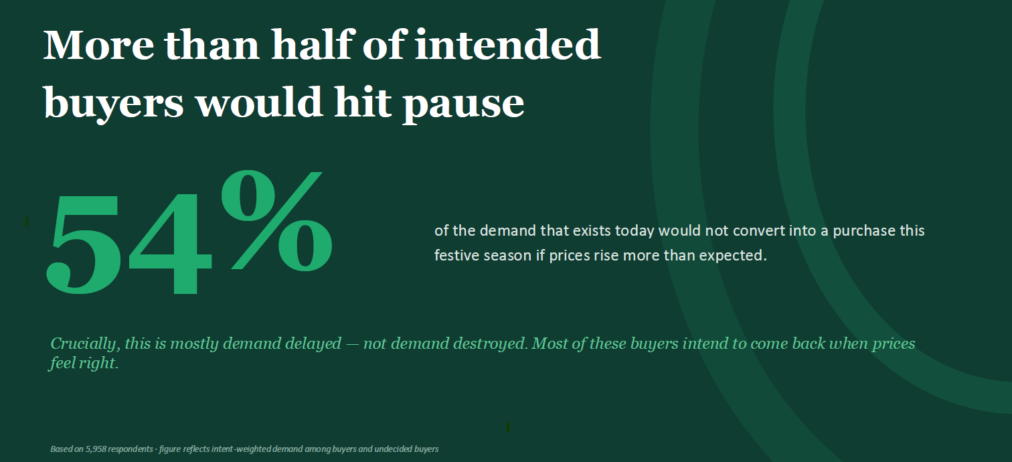

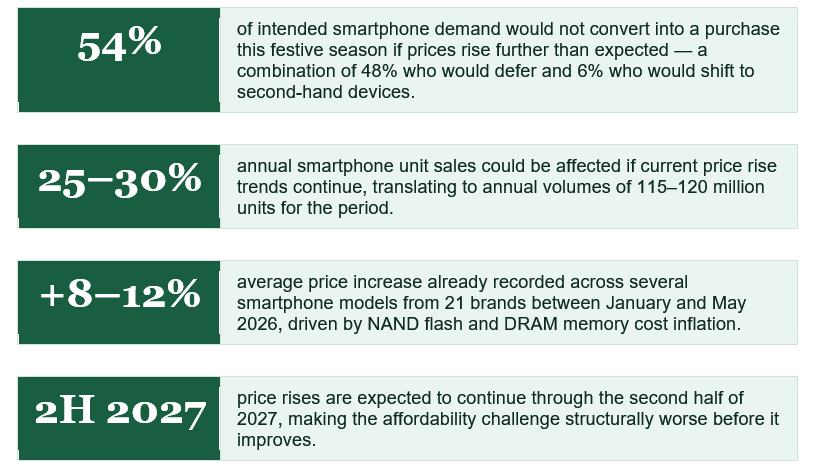

Pan-India study of 5,958 smartphone buyers finds that more than half of intended purchases would be deferred or redirected to the second-hand market if prices rise further, with memory cost inflation set to continue driving prices upward through the second half of 2027.

Gurugram/Pune/Srinagar: May 29, 2026: Trakin Tech, India’s leading consumer technology media platform, and Techarc, a premier technology analytics and research firm, today released a major joint study on Indian smartphone consumer behaviour in a rising price environment. The report, “What Will India Do if Smartphones Keep Getting Pricier?” is based on a survey of 5,958 active smartphone buyers across India and reveals a market at a critical inflection point.

Key Findings at a Glance

The Context: A Structural Price Shock

India’s smartphone market is navigating an unprecedented cost environment. Global NAND flash and DRAM memory costs surged through 2025–26, forcing OEMs to reprice models across all price tiers. Entry and budget segment handsets have borne the steepest increases, with prices rising 8–12% on average since launch for the sub-₹20,000 segment, where memory costs form a disproportionately large share of the bill of materials, as high as 40%.

Consumer Response: Five Paths, Two Drive Erosion

The study asked 3,116 festive half (Jul-Dec 2026) intended buyers how they would respond if smartphone prices rose higher than their expectations. Five distinct responses emerged:

- Wait and watch (48%): The largest cohort would simply postpone the purchase until prices settle. Critically, this represents delayed demand, not destroyed demand.

- Settle for less (22%): Buyers would proceed but step down on specifications to stay within budget.

- Buy anyway (17%): A determined segment would go ahead regardless of price.

- Pay over time (7%): EMI and instalment-based purchase would be the chosen route.

- Go second-hand (6%): Buyers would shift to refurbished or pre-owned devices entirely.

The 48% who defer and the 6% who go second-hand together constitute the 54% demand erosion figure. The silver lining: the vast majority of deferrers intend to return to the market when prices feel right, making the festive season window a critical conversion opportunity.

Vulnerable and Resilient Segments

The study reveals significant variation in price sensitivity across age groups and device price tiers:

- Most vulnerable age cohort: Buyers aged 35–44 have the highest deferral rate at 54.8%, driven by competing financial priorities such as EMIs, children’s expenses, and household costs.

- Most resilient age cohort: Buyers aged 18–24 defer at just 43.1%, the lowest of any age band, and are the most aspirational receptive segment. They represent the industry’s most critical growth opportunity.

- Most resilient price segment: Owners of ultra-premium devices (above ₹1 lakh) defer at only 30.9% and buy regardless at 44.4%, the most defensible demand pocket in the market.

- Most fragile price segment: The ₹15,000–30,000 mid-range segment carries the highest absolute deferral volume, with 22% of buyers in this band choosing to ‘downtrade’ rather than wait.

Six Buyer Archetypes Redefine Market Segmentation

The study identifies six behavioural archetypes that cut across demographics and define what the industry must do differently for each buyer group:

- Frustrated Waiters (31%): Need a new phone but are being held back by price. The largest and most immediately convertible group.

- Aspirational Climbers (20%): Want to upgrade to a better phone and will adjust their budget to do so.

- Patient Deferrers (17%): In no hurry. They will wait for the right moment or offer.

- Determined Buyers (11%): Will buy regardless of price. High value, low intervention required.

- Finance-First Buyers (10%): Will purchase only if EMI makes it manageable.

- Second-hand Curious (6%): Open to refurbished or pre-owned as a way to save.

Brand Resilience: Apple and One Android Brand Stand Apart

The study’s brand resilience analysis, measuring the share of each brand’s buyers who would still proceed with a purchase despite a price rise, reveals a clear two-tier structure. Apple scores a commitment index of 54 and stands as the clear resilience benchmark: only 43.2% of iPhone buyers defer, and 24% say they will pay regardless of price.

Among Android brands, only one brand, with a commitment score of 55, sits in the same resilience zone as Apple. The remaining Android brands cluster in the 41–49 range, with no brand in the below-30 (most price-sensitive) zone this year. This means most of these Android brands will bear similar impact on their demand and sales.

How the Market is Changing

The study highlights four structural shifts that will define the market tomorrow:

- Youth-led: 57% of respondents are aged 18–24 and students form 46% of the base. This cohort defers the least and is highly brand-aspirational and EMI-receptive.

- Experience over specs: Camera (60%), battery (57%) and processor (54%) top upgrade priorities. Pure specification upgrades are losing relevance; experiential improvements drive decisions.

- Mid-tier under pressure: The ₹15,000–30,000 segment has the highest absolute deferral volume (727 units at risk in the study sample). It is the single most contested battleground.

- Finance and refurb going mainstream: Past EMI users are 3.5x more likely to use EMI again. 6.3% of buyers are now open to refurbished, a channel brands can no longer afford to ignore.

SPOKESPERSON QUOTES

Arun Prabhudesai, Founder, Trakin Tech

“The message from Indian consumers is loud and clear: they still want better smartphones, but not at any price. If prices continue to rise, buyers will wait, compromise, finance, or move to refurbished devices. This is a wake-up call for every smartphone brand. India’s next growth cycle will not be won only by better specs; it will be won by brands that make technology feel affordable again.”— Arun Prabhudesai, Founder, Trakin Tech

Faisal Kawoosa, Founder & Chief Analyst, Techarc

“This year it has become extremely critical for smartphone brands how they approach the festive season. The intended buyers show divergently different signs of resilience and cohort behaviours which the brands need to bedrock their strategy on. The era of ‘one size fits all’ is over. It is time for smartphone brands to listen to buyers and design a cohort-based blueprint.”— Faisal Kawoosa, Founder & Chief Analyst, Techarc

Strategic Implications for the Industry

The study concludes with a three-point strategic framework for the industry:

- Demand is delayed, not gone. The 54% erosion is recoverable. A well-timed festive push — with the right offer for the right archetype — can win much of it back.

- The festive window is decisive. With nearly half of all intended buyers waiting for prices to settle, the festive season becomes the single most important moment in the 2026 demand calendar.

- Segment and stratify, not one playbook for all. Ultra-premium, young aspirational buyers and Tier-2/3 city consumers are resilient pockets to be leveraged. Senior millennials in the mid-range are fragile pockets that require targeted intervention.

The report also introduces a 4P Blueprint framework, Product, Price, Place, Promotion, recommending that each brand cross-analyse the emerging market condition with its own portfolio, channel strengths and the brand-specific vulnerabilities identified in the survey.

ABOUT

About the Report

“What Will India Do if Smartphones Keep Getting Pricier?” is a joint study by Trakin Tech and Techarc on Indian smartphone consumer behaviour in a rising price environment. The study surveyed 5,958 active smartphone users across India, covering 11 major smartphone brands across metro, Tier-2 and rural geographies, in English and Hindi. Headline findings are reported at the 95% confidence level with a margin of error of ±1.3 percentage points for the full sample. Brand-level findings are indicative; subsample sizes vary by brand. The study is designed to represent the engaged, online smartphone buyer in India and is not a census of all phone owners. Brand strategy playbook reports are available on request.

About Trakin Tech

Trakin Tech is one of India’s leading consumer technology media platforms, covering smartphones, gadgets and consumer tech for millions of followers across YouTube, social media and digital channels. Founded by Arun Prabhudesai, Trakin Tech is known for independent, accessible technology journalism that reaches and influences India’s largest and most engaged tech buyer audience. For more information, visit www.trakintech.com.

About Techarc

Techarc is a premier technology analytics, research and consulting firm specialising in the Indian device, telecom and consumer technology market. Founded by Faisal Kawoosa, Techarc provides data-driven intelligence to brands, investors and policymakers navigating India’s dynamic technology landscape. Techarc’s proprietary trackers — including the Smartphone Price Change Tracker and the Techarc Consumer Sentiment Index — are reference tools for the Indian technology industry. For more information, visit www.techarc.net.

Media Contact

For press queries, interview requests or a copy of the full report, please write to:

info@techarc.net

insights@trak.in

Note to editors: All figures cited in this release are from the Trakin Tech × Techarc joint study, May 2026. The 54% demand erosion figure reflects intent-weighted demand among buyers and undecided buyers (base: 3,116). The 25–30% annual sales impact is an extrapolation based on 2H sales figures factoring the demand erosion in planned purchases during the festive period.