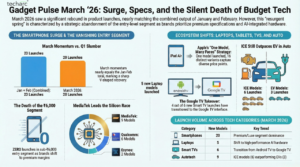

The first quarter of 2026 establishes a polarizing narrative across the consumer technology landscape. Broadly, we are observing a lean portfolio of gadgets characterized by an upward shift in product positioning, which is driving up Average Launch Price (ALP) across the personal computing and mobile sectors. Manufacturers are navigating increased supply chain constraints by prioritizing higher-margin devices over sheer volume. Conversely, the smart TV market is experiencing severe price compression, fueled by intense competition among newer entrants and faster adoption of advanced features at lower tiers.

Key Takeaways

- The Death of the Budget Tier: Rising component costs have forced manufacturers to abandon sub-₹10K smartphones and entry-level laptops, officially making the ₹10K–₹20K Base tier the new market floor.

- Variant Expansion Replaces Base R&D: To control development costs, manufacturers are releasing fewer base models but multiplying them into dozens of variants to micro-target specific price bands.

- Divergent Screen Economics: While personal devices (smartphones, laptops) are facing severe price inflation, smart TVs are experiencing rapid price compression, with advanced tech like QLED becoming standard at entry-level tiers.

- A Bifurcated Tablet Market: The massive surge in tablet Average Launch Prices (from ₹31.5K to ₹82.5K) is driven entirely by Apple’s ultra-premium positioning, while Android OEMs compete strictly in the sub-₹50K space.

Here is the sector-by-sector strategic breakdown for Q1 2026.

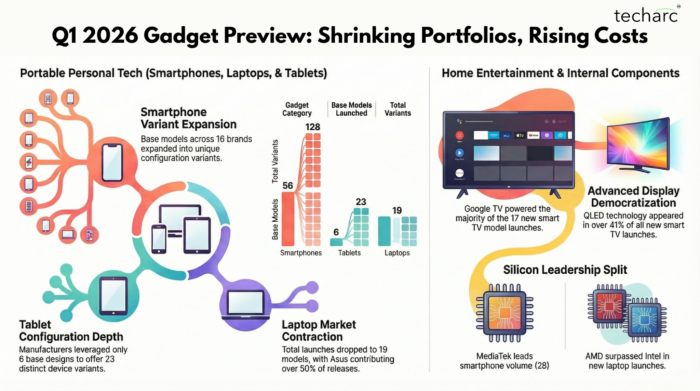

1. Smartphones: A 26% ALP Surge and Entry-Tier Contraction

Smartphone launch volumes increased from 48 models in Q1 2025 to 56 models this quarter. The manufacturer strategy shifted from sheer model volume to configuration depth, with those 56 models yielding 128 variants across 16 brands. Deploying 128 variants allows manufacturers to establish a presence across multiple micro-price bands, maximizing market coverage without the R&D expenditure required to develop distinct base hardware.

The primary macroeconomic indicator is the inflation of the Average Launch Price (ALP), which now sits at ₹39.2K, a 26% year-over-year increase from ₹31K.

Pricing Cohort Analysis: The industry is shifting focus away from the bottom of the pyramid to offset rising component costs, particularly memory and storage modules.

1.1 Pricing Segment Analysis

The sub-₹10K entry tier is fading rapidly as brands shift their focus upward, effectively bypassing the budget segment to target a higher-spending cohort.

- Entry (Below ₹10K): Only 4 were launched in this segment, and these are mostly 4G Models. The segment is currently sustained primarily by iTel (2 models), with Realme (1) and Tecno (1) providing the remaining options.

- Base (₹10K–₹20K): This segment recorded the highest volume with 18 launches, indicating a clear strategic shift toward this price band. Samsung, Oppo, and Vivo lead with 3 launches each. Realme, Poco, and Lava follow with 2 each, while Redmi, Tecno, and iQOO contributed 1 each.

- Mid (₹20K–₹30K): A solid segment with 8 launches, led by Realme and Redmi (2 launches each). Vivo, Infinix, Tecno, and Motorola each added 1 launch.

- Premium (₹30K–₹50K): The second-largest segment of the quarter with 14 launches, cementing the industry’s premiumization trend. Poco leads the pack (3 launches), followed by Oppo, Realme, and Nothing (2 each). Vivo, iQOO, Redmi, Motorola, and Samsung each contributed 1 launch.

- Super Premium (₹50K–₹100K): This high-end tier saw 9 launches. Samsung, Vivo, and Oppo have 2 each, while Xiaomi, Motorola, and Apple round out the category with 1 launch apiece.

- Luxe (Above ₹100K): The ultra-premium category saw 3 exclusive launches, dominated by Samsung (2) and Xiaomi (1).

1.2 Silicon Strategy

- MediaTek leads in volume (28 launches), maintaining a high concentration in the Base and Mid tiers, where device volume is highest.

- Qualcomm (16 launches) retains its share in the higher segments, powering 9 models in the Premium tier.

- Proprietary Processors: Samsung’s Exynos (4 devices) competes closely with Unisoc (5 devices) in the lower-to-mid tiers, indicating a continued push for vertical integration to control hardware costs.

2. Laptops: A Contracting Consumer Market Focuses on Larger Displays

The consumer laptop market contracted, with new model launches dropping from 29 in Q1 2025 to 19 across 5 brands this quarter. This contraction aligns with elongated replacement cycles in the consumer space following previous purchasing surges. With overall volume shrinking, OEMs are prioritizing higher-priced, large-format devices to maximize revenue per unit.

2.1 Brand & Segment Dynamics

- Asus leads the quarter with 10 new launches, capturing the bulk of the consumer release cycle, while Apple (4) and Samsung (3) maintain targeted, specialized portfolios.

- The pricing strategy mirrors the smartphone market: the Premium and Luxe segments account for 63% of all new launches (12 out of 19), significantly limiting consumer options in the entry and base tiers.

2.2 Form Factor & Silicon Shifts

Manufacturer preference leans heavily toward desktop replacement form factors over ultra-portability.

- 16-inch displays are the primary focus, representing 11 launches, followed by 14-inch (7 launches) and 15.6-inch (4 launches) displays. This shift reflects a consumer preference for larger screen real estate to accommodate hybrid work and multimedia consumption.

- In processors, AMD surpassed Intel in this quarter’s consumer launch cycle, powering 9 devices to Intel’s 6. Apple accounted for 4 launches with its proprietary silicon.

3. Tablets: The Apple Skew and Variant Expansion

The tablet market exhibited a notable structural shift. While base model volume remained flat year-over-year (6 models), OEMs increased configuration options, resulting in 23 distinct variants. This extensive variant strategy indicates a push to maximize the return on investment for base hardware designs.

3.1 The Pricing Anomaly

The market ALP increased from ₹31.58K in Q1 2025 to ₹82.58K. This upward skew is heavily influenced by Apple. Positioned above the ₹100K mark, Apple’s high-priced variants elevate the overall industry average.

3.2 This establishes a bifurcated market

Apple operates in an isolated high-margin tier, while Android manufacturers (Xiaomi, Brave, Realme, Oppo, and Redmi) are positioned strictly below the ₹50K threshold, capturing the Mid (50%) and Premium (33.3%) tiers. This indicates Android OEMs are currently avoiding direct competition at the highest price points. Qualcomm leads the Android tablet processor space, powering 3 of the 6 new models.

4. Smart TVs: Price Compression and the Democratization of Tech

In contrast to the upward price shifts in personal computing, the smart TV market is undergoing aggressive price compression. Launch volumes contracted from 26 models to 17, but the defining metric is the reduction in the Average Launch Price.

4.1 The Drop in TV ALP

The TV ALP decreased from ₹61.66K in Q1 2025 to ₹27.51K. OEMs shifted their focus away from high-priced launches in Q1, pivoting toward Entry and Mid-range tiers, which now account for over 70% of the market.

- Xiaomi is the sole outlier, with a launch near ₹70K, while the majority of the market operates below ₹40K. The presence of volume drivers like Tivora (3), Wobble (3), and RGL (2) indicates a highly fragmented lower tier where aggressive pricing is the primary competitive tool.

4.2 Ecosystem & Hardware Democratization

- Google TV powers the majority of the market (9 of the new models), leading standard Android and alternative OS platforms like webOS and JioTele OS. This standardization reduces software development costs for manufacturers.

- Advanced display technology is now standard at lower price points. While standard LED represents 47.06% of launches, QLED accounts for 41.18%. The rapid integration of QLED technology into lower tiers points to maturation in panel manufacturing and supply chain efficiencies, effectively altering the baseline specifications expected by consumers.

5. Conclusion & Outlook

Looking ahead to the remainder of 2026, the consumer electronics market is entering a phase characterised by margin protection over sheer volume growth. Manufacturers in the mobile and laptop sectors will continue to leverage configuration depth to capture higher-spending cohorts, effectively pricing out the traditional budget buyer.

As the entry-level tier evaporates and ALPs rise, we anticipate a subsequent elongation of the device replacement cycle. Consumers faced with a less for more value proposition will likely hold onto their existing smartphones and laptops for longer periods.

Conversely, the smart TV segment is positioned for high turnover but severe margin pressure. The democratization of Google TV and QLED panels at the ₹27.5K average price point leaves TV manufacturers with very little room for hardware differentiation. Throughout the rest of the year, we expect TV OEMs to shift toward software monetization and ad-supported interface models to recoup the hardware margins lost in this current race to the bottom.