Gurugram/Srinagar, May 15: India’s telecom sector did not evolve, it detonated, rebuilt, and detonated again. A comprehensive decade-long analysis of the industry, spanning Q1 2015 to Q4 2025, identifies ten defining moments that irrevocably reshaped every metric, from who holds a SIM card to what an operator earns per subscriber.

- The 10 Moments That Changed Everything

- The first shock arrived on 5 September 2016, when Reliance Jio launched with free voice calls and 4G data at sub-paisa rates. India added 15.98 million Jio SIMs in a single quarter. ARPU, sitting at ₹121, began a long, brutal slide. Within months, the industry was in crisis, and the mergers began.

- By March 2017, Vodafone and Idea announced a defensive merger, pooling approximately 204 million and 191 million subscribers, respectively, for a combined market share of roughly 33%. Bharti-Telenor and Bharti-Tata Teleservices deals followed in the same quarter.

- March 2018 delivered the first casualty. Aircel, once a top five operator with a peak of ~91 million subscribers, filed for insolvency before the NCLT, its ARPU having collapsed to ₹76. One player down; others would follow.

- On 31 August 2018, the Vodafone-Idea merger completed, creating Vi with 435.22 million subscribers and a 36% day-one market share. But what looked like strength was structural fragility, subscriber count fell to 333 million by Q4 2019 as users migrated en masse to Jio and Airtel.

- The Supreme Court’s AGR verdict on 24 October 2019 imposed cumulative dues of approximately ₹1.4 lakh crore on telcos, covering spectrum and licence fees on non-telecom revenue. Airtel posted a net loss of ₹23,045 crore in a single quarter. The entire industry stood on the edge.

- Then came COVID. The national lockdown of March–April 2020 did the unexpected: it legitimised telecom as essential infrastructure. Average data consumption per user crossed 12.15 GB per month. Wired broadband subscriber count touched approximately 22 million and began its first genuine growth curve, rising over 15% year-on-year.

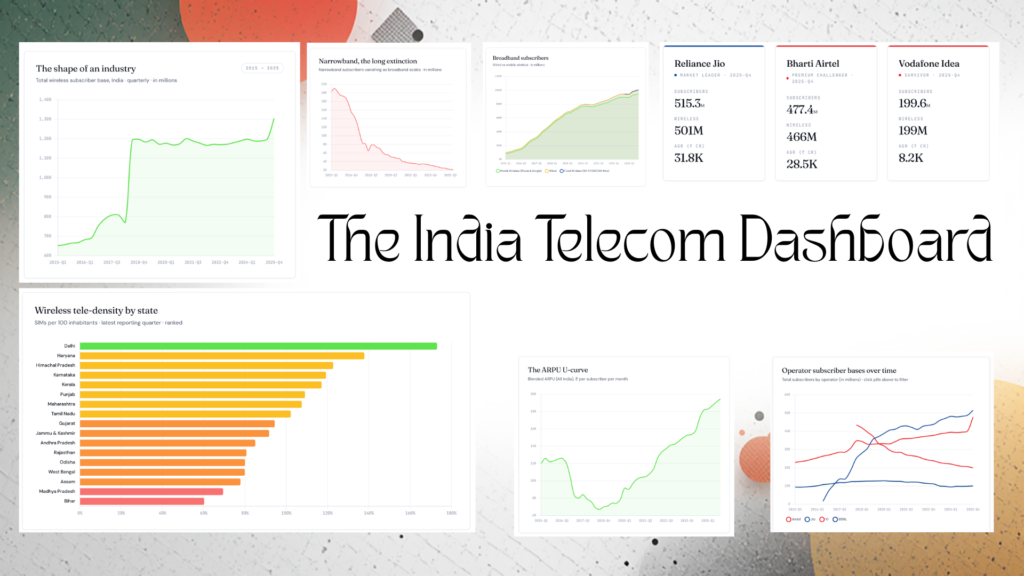

- Click the above image to view the India Telecom Dashboard

- The government responded to sector-wide stress with a reform package in September 2021, a four-year moratorium on AGR and spectrum dues, an ~80% cut in bank guarantees, and a prospective redefinition of AGR excluding non-telecom revenue. It was a lifeline delivered as a policy reform.

- November–December 2021 brought the first tariff hike in five years. All three private operators raised prepaid plans by 20–25%. ARPU crossed ₹100 for the first time since Jio’s arrival, reaching ₹114, up 63% from Q4 2018 lows. The tariff repair era had begun.

- October 2022 marked India’s 5G inflection. Reliance Jio and Airtel launched commercial 5G simultaneously, Jio on standalone architecture, Airtel on non-standalone, covering 8 cities on day one and expanding to over 700 cities within a year. Average data consumption had climbed to 17.11 GB per user. Vi sat out; BSNL’s 4G remained pending.

10. The second and decisive tariff correction came in July 2024, when Jio, Airtel, and Vi raised tariffs by 10–25% in a coordinated post-election move. ARPU crossed ₹172 that quarter and continued climbing, reaching ₹194.57 by Q4 2025, the highest in over a decade.

- The Journey in Numbers

Subscribers: Total wireless subscribers now stand at approximately 1.3 billion. From a 12-operator landscape in 2015, the market has consolidated into three private operators and two PSUs.

Revenue & ARPU: Blended ARPU for private operators reached ₹203.86 in Q4 2025, with data usage averaging 25.7 GB per user per month, a 100x increase from the 0.23 GB recorded in Jio’s launch quarter.

Internet & Data: Mobile broadband subscribers have grown from roughly 92 million in mid-2015 to well over 900 million today, driven almost entirely by mobile wireless. Wired broadband, long stagnant, now shows consistent quarterly additions.

Operator Battle: Reliance Jio commands 39.47% market share with 515.3 million subscribers. Bharti Airtel holds 36.56% with 477.41 million subscribers and is closing the gap rapidly. Vodafone Idea has declined to 199.59 million subscribers (15.29%), while BSNL holds 100.24 million (7.68%).

Geography: Penetration remains uneven. Ladakh leads with a tele-density of 177.53%, Chandigarh at 137.3%, while states like Dadra & Nagar Haveli and Tripura remain under 85%. Uttar Pradesh (East) alone accounts for 109 million wireless subscribers, larger than most countries’ entire subscriber base.