Analysis of 79 models, 21 brands across 6 price tiers | Launched between Jan – Jun 2025

India’s smartphone market underwent a significant repricing cycle between January 2025 and May 2026, driven by global NAND flash and DRAM memory cost inflation. Techarc tracked 79 models across 21 brands across six price tiers from Entry (

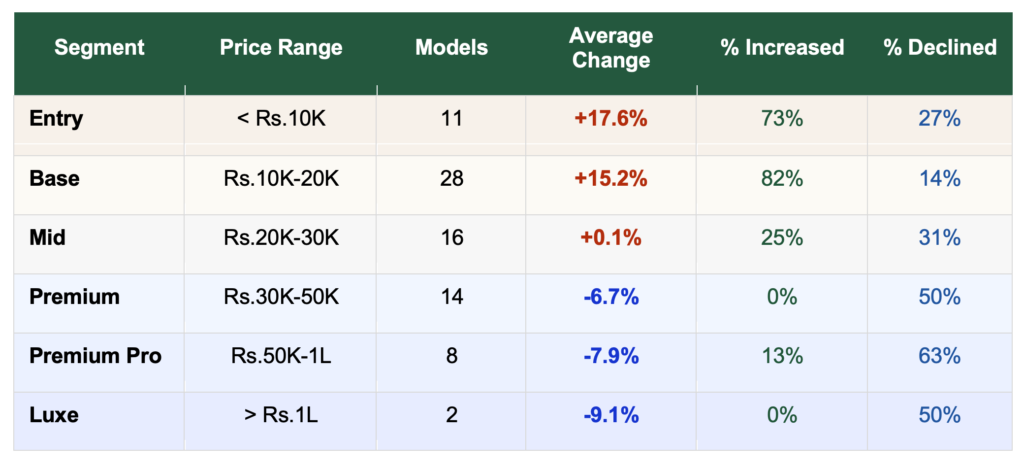

A defining finding is the sharp divergence between value and premium. Entry-tier models rose an average of +17.6% and Base-tier climbed +15.2%, while Premium Pro and Luxe models declined by 7-9% as brands competed aggressively for high-income buyers. This bifurcation defines Indian smartphone pricing in 2025-26.

The V-Curve: How the Memory Shock Arrived

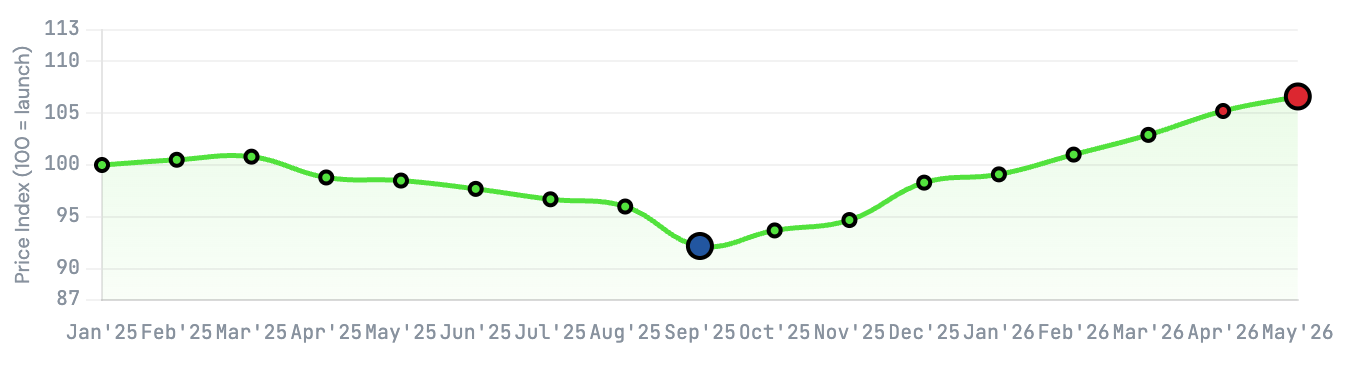

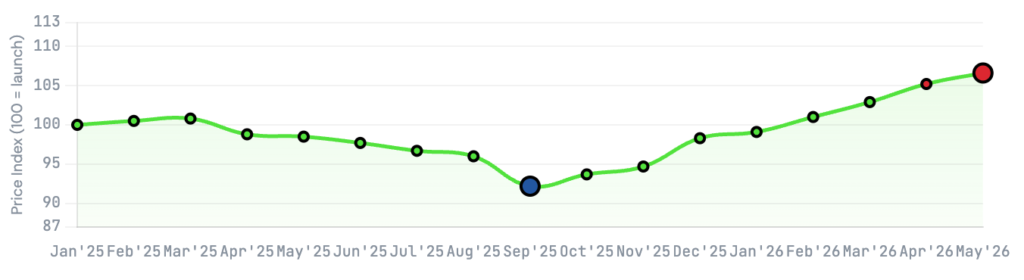

Prices held firm near launch levels through Q1 2025 before a gradual descent driven by e-commerce discounting. By September 2025, the Techarc Price Index bottomed at 92.2, meaning the average handset was trading nearly 8% below its launch price. The reversal began in Q4 2025 as global memory contract prices rose. By May 2026, the index climbed to 106.6 — a 14.4-point swing representing the sharpest industry-wide repricing in recent memory.

The V-curve was not symmetric. Prices fell slowly and rose sharply. September 2025 marks the inflection point where memory cost pressures fully transmitted into the retail channel, particularly for budget-tier devices where memory represents a larger share of BOM.

Segment Analysis: Entry to Luxe

Techarc’s six-tier framework reveals the full picture of divergent price trajectories:

Three structural conclusions emerge: (1) Entry and Base tiers are the new BOM battleground, with most models rising as brands passed through memory costs; (2) Mid-tier is a transition zone, effectively flat as models split between modest increases and declines; (3) Premium and above compete on share, not margin, with prices moving down as brands target high-value consumers with multiple choices.

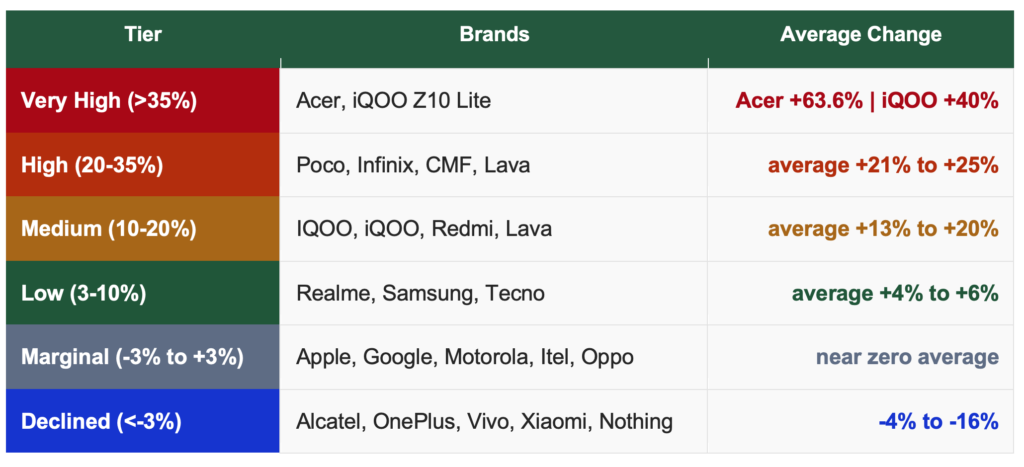

Brand Heatmap: Six Tiers of Price Behaviour

Techarc categorised all 21 brands into six tiers by weighted average price change:

Three brand narratives define the period:

- Poco’s aggressive repricing. Average +24.4% across four models, highest among multi-model challengers. The X7 Pro’s peak price entered flagship territory.

- Samsung’s internal bifurcation. +5.4% average hides enormous variance — Galaxy M16 5G rose +39.1% while Galaxy S25 fell -16.9%. Entry/Base models absorb costs; flagships absorb competition.

- Apple and Google hold firm. iPhone 16e at 0.0% and Pixel 9a at -0.1% confirm ecosystem-locked brands don’t need to move retail prices during cost cycles.

Notable Outliers

High outliers — price rise >35%

- Acer Super ZX 5G (+63.6%): Rs.10,999 to Rs.17,999 (Base). Single-model brand with volatile pricing; statistically notable but limited market signal.

- iQOO Z10 Lite 5G (+40.0%): Rs.9,999 to Rs.13,999 (Entry). Systematic 11-month hike; strongest evidence of memory cost passthrough at budget-5G tier.

- Samsung Galaxy M16 5G (+39.1%): Rs.11,499 to Rs.15,999 (Base). Moved up an entire price tier; now competes in Mid rather than Base.

- Redmi A5 (+36.2%): Rs.6,499 to Rs.8,849 (Entry). Entry-level repricing; dramatic for a sub-Rs.9K device.

- Motorola G05 (+35.8%): Rs.7,361 to Rs.9,999 (Entry). Notable against Motorola’s brand average of -0.6%.

Declining outliers — price drop >15%

- Realme GT 7T (-25.6%): Rs.37,609 to Rs.27,999 (Premium). Sharpest single-model decline; repositioned into Mid segment.

- Motorola Edge 60 Pro (-20.8%): Rs.36,990 to Rs.29,285 (Premium). Consistent monthly erosion driven by Poco and iQOO pressure.

- Motorola Razr 60 Ultra (-20.0%): Rs.99,999 to Rs.79,999 (Premium Pro). Flagship foldable category under pressure from Samsung.

- OnePlus 13 (-17.1%): Rs.69,998 to Rs.57,999 (Premium Pro). Nearly Rs.12,000 decline driven by competitive discounting.

Techarc View

The 2025-26 memory price cycle exposed a fundamental asymmetry: the segment most exposed to component cost inflation is also least able to resist it. Entry and Base buyers are price-sensitive, have limited brand loyalty buffers, and buy devices where memory represents a larger BOM share — making them the primary absorbers of the global memory supply shock.

- Budget 5G is the new cost-absorption battleground. As sub-Rs.20K devices expand memory footprints for 5G and camera ISPs, BOM sensitivity grows. Brands without procurement scale in Entry and Base segments face continued margin pressure even when memory prices stabilise.

- Premiumisation is a structural hedge. Premium Pro and Luxe data confirms that brands with significant revenue above Rs.50,000 can absorb memory cycles without retail price moves. The brands moving deliberately up-market are making a structurally sound risk-management decision.

- Price volatility will cost challenger brands mindshare. Poco, Infinix, CMF, and iQOO — all averaging increases above 20% — are recalibrating their value propositions. Without clear consumer communication, price hikes risk being perceived as broken promises by buyers who chose these brands specifically for aggressive pricing.

Techarc expects memory prices to soften modestly after H2 2027. However, given the pricing normalisations already embedded in the market — especially in the Rs.8,000 to Rs.18,000 band — a meaningful return to pre-cycle price levels is unlikely. The new pricing floors in Entry and Base are likely to hold, making the Rs.10,000 to Rs.15,000 band significantly denser with feature-competitive devices than 18 months ago.