The consumer electronics industry witnessed a significant surge in product launches during April 2026. While activity accelerated across smartphones, smart TVs, and laptops compared to the previous year, the overarching trend points to a noticeable shift away from budget-friendly options. Driven by rising component costs, the Average Launch Price (ALP) is climbing steadily, raising concerns for budget-conscious consumers, particularly in the PC and mobile sectors.

Key Takeaways

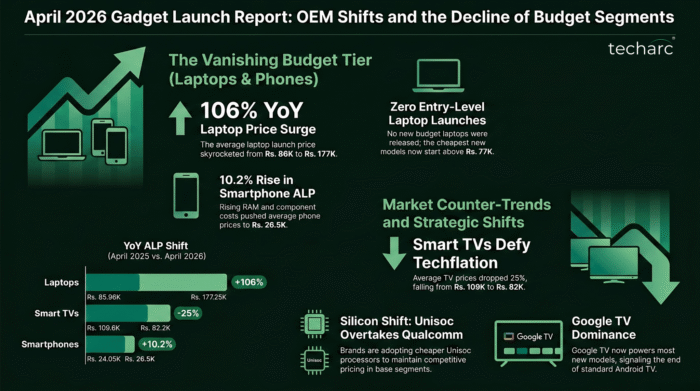

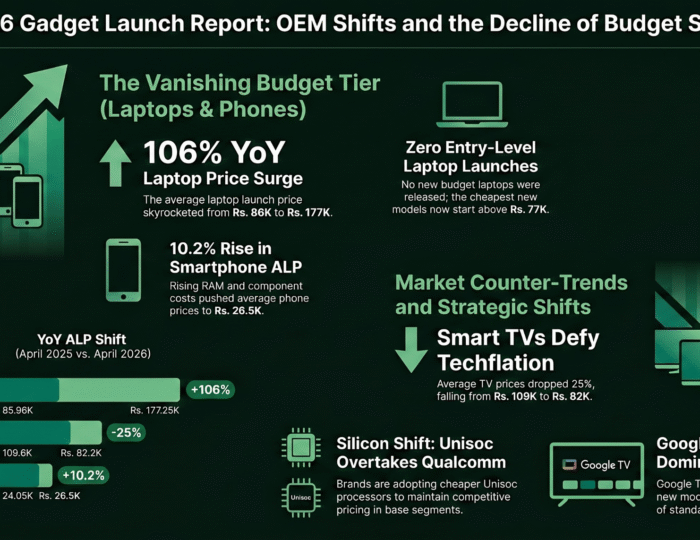

- Laptops Abandon the Budget Tier: A staggering 106% YoY price surge (ALP Rs. 177K) and absolutely zero entry-level launches mean budget laptop buyers are effectively priced out of the new market.

- Smart TVs Defy Techflation: Bucking the trend of rising costs, TVs became much more affordable (ALP dropped from Rs. 109K to Rs. 82K), with OEMs actively pushing accessible QLED and Google TV options.

- Mobile Silicon Shakeup: Unisoc unexpectedly overtook Qualcomm for second place in smartphone chipsets, proving that brands are heavily leaning on cheaper processors to combat rising component costs in base segments.

Here is a detailed breakdown of the market activity and segment distributions for April 2026.

1. Smartphone Launches: Incremental Price Hikes

The smartphone industry saw 22 new models launched across 12 brands, featuring 43 different RAM/ROM configurations. This marks a clear increase in market activity compared to April 2025, which saw only 15 models from 10 brands.

1.1 Brand Leadership: Redmi led the pack with 4 new launches, followed by Ai+ with 3. Lava, Oppo, realme, Poco, and vivo launched 2 models each. Motorola, Infinix, iQOO, OnePlus, and Tecno rounded out the month with 1 launch apiece.

1.2 Segment Focus: The Base segment drove the most volume with 9 launches, closely followed by the Premium segment with 8. The Entry segment saw only 3 launches, while Mid and Premium Pro had 1 each. There were no new Luxe segment devices.

1.3 Chipset Market Contribution: MediaTek lead the month powering 9 devices. Surprisingly, Unisoc secured the second position with 8 launches (powering devices for Redmi, Ai+, Lava, and Poco), pushing Qualcomm down to third place.

1.4 Average Launch Price (ALP): The ALP for the month settled at Rs. 26.5K, up from Rs. 24.05K in April 2025. While seemingly marginal, this 10.2% increase is a noticeable bump directly attributed to the rising costs of components and RAM in 2026.

2. Smart TV Launches: The Exception to the Rule

Bucking the trend of rising prices, the Smart TV sector proved to be highly accessible this month. Manufacturers released 30 variants across 12 brands, a massive jump demonstrating accelerated activity when compared to the 17 models launched in the entirety of Q1 2026.

2.1 Brand Leadership: realme led the category with 5 launches. LG and Samsung followed with 4 each; Motorola had 3; Lumio and Toshiba launched 2 each. Brands like Akai, Coocaa, Croma, Onida, Skylive, and Xiaomi released 1 model each.

2.2 Segment Focus: The Mid segment was the primary focus with 12 launches. The Premium segment saw 7 launches, Entry had 4, and the Luxe segment saw 3.

2.3 Display Technology: QLED displays dominated, accounting for 50% of all new launches. Mini LED followed with 26.92%, QNED with 15.38%, and standard LED trailing at just 7.9%.

2.4 Operating Systems: Google TV has established near-total dominance, powering 16 of the 26 base models. Tizen and WebOS powered 4 models each. Legacy Android TV and Fire TV saw only 1 launch each, signalling a definitive phase-out of standard Android TV interfaces as predicted.

2.5 Average Launch Price (ALP): Smart TVs saw a notable decrease in pricing. The ALP for April 2026 stands at Rs. 82.2K, down significantly from Rs. 109.6K in April 2025. The current market offers a massive price matrix, starting as low as Rs. 11.5K and scaling up to Rs. 599K for premium Samsung units. This signals that OEMs are actively maintaining options for every category of buyer rather than exclusively pushing premium models.

3. Laptop Launches: The Death of the Budget Tier

Following a sluggish first quarter that experienced a 34% decline in overall launch volume, April brought 19 new laptop models and variants across 4 brands. However, the industry has heavily pivoted toward high-end computing, leaving entry-level buyers with virtually no new options.

3.1 Brand Leadership: Asus dominated the month with 8 new models. Lenovo followed with 5, Dell released 3, and MSI rounded out the group with 2.

3.2 Segment Focus: The Premium segment accounted for nearly half the market with 9 launches. Mid and Luxe segments saw 4 launches each. The Base segment saw merely 1 launch, and there were absolutely zero Entry-level launches.

3.3 Processor Market Share: Intel showcased absolute dominance, powering 14 of the 18 new models and leaving very little room for competitors. Qualcomm secured a distant second with 3 launches, while AMD powered only 1, indicating an increasingly tough competitive landscape for non-Intel OEMs.

3.4 Average Launch Price (ALP): The most concerning data for consumers is the staggering 106% year-over-year ALP increase in the laptop sector. The average price for April sits at Rs. 177.25K, compared to just Rs. 85.96K in April 2025. With the absolute lowest-cost new laptop starting above Rs. 77K and the bulk of new hardware concentrated in the >100K segment, budget-constrained PC buyers are effectively being pushed to the edge.

4. Tablets

This month saw a normalized trend with 3 tablet models launched, comprising 4 variants across 3 brands. In contrast, March saw 4 model launches with a staggering 18 variants, primarily driven by the iPad Air’s 16 different configurations.

4.1 Segment Distribution: Of the 3 models launched, two are positioned in the premium segment, while the remaining one targets the entry-level segment.

4.2 Brand Presence: The brands that launched these 3 models are OnePlus (1 model with 2 variants), Ai+ (1 model), and Lenovo (1 model).

4.3 Processor Distribution: Qualcomm leads the pack, powering 2 out of the 3 tablets, while the remaining model is powered by MediaTek.

4.4 Average Launch Price (ALP): The overall Average Launch Price (ALP) has dropped to Rs. 37.5K, down from Rs. 41K during the same period last year (April 2025).

5. Conclusion

The April 2026 consumer electronics market reveals a stark divergence in OEM strategies. Driven by rising component costs, smartphone and laptop manufacturers are increasingly abandoning budget-friendly tiers in favor of high-margin, premium devices, effectively pricing out entry-level buyers. Conversely, the Smart TV sector is democratising advanced technology, offering highly accessible pricing and driving massive volume. Ultimately, as new entry-level Laptops and smartphones become scarce, budget-conscious consumers will likely be forced to shift toward the growing tablet market or rely heavily on refurbished hardware.