The TWS earbud brands have done a remarkable job of expanding the market of this wearable category, which also picked up during COVID-19, as every user wanted their own space working from home. But there is a general dissatisfaction among users in the sub ₹10,000 category reveals Techarc’s report analysing the customer acceptance of TWS earbuds in the entry to mid-tier segments.

By analysing this data, clear systemic vulnerabilities and functional gaps emerge, highlighting a market that is ripe for disruption by brands willing to prioritize technical fundamentals over sheer volume.

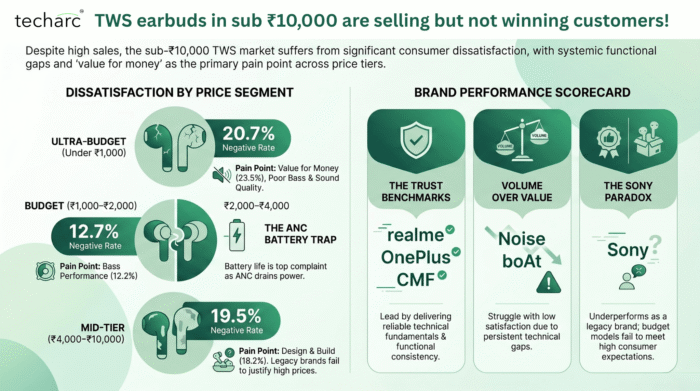

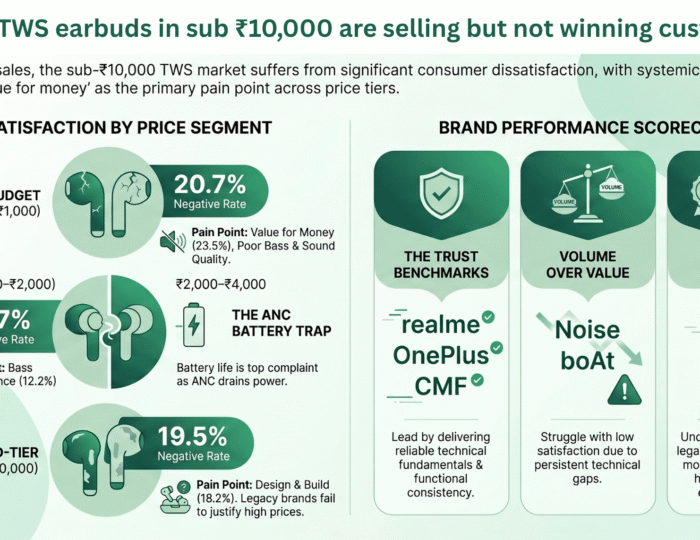

1. The Perceived Value for Money Paradox

The overarching driver of consumer dissatisfaction in the sub-₹10,000 category is a fundamental failure to justify the price-to-performance ratio.

- While premium buyers often pay a brand tax for prestige, entry and mid-tier consumers are strictly driven by functional utility. They purchase TWS products expecting specific technical capabilities.

- A significant segment of dissatisfied users (averaging 20%) report that current market offerings fail to justify their cost. When these consumers encounter compromised functionality, brand equity offers no protection against severe dissatisfaction. The data confirms that delivering quantifiable value is actually more critical in the budget and mid-tiers than in the premium segment.

2. Doubling down the critical gaps

- Below ₹1,000 (Average Negative Rate: 20.7%): This volume-heavy segment is led by brands like Noise, yet it suffers from universal underperformance. Consumers feel the products fail to justify even their minimal cost. The top pain points in this segment are as value for Money (23.5%), Bass Performance (20.5%), and Overall Sound Quality (20.2%).

- ₹1,000–₹2,000 (Average Negative Rate: 12.7%): This is the highest-performing segment in the market, heavily stabilised by brands like OnePlus and realme, who have set strict industry baselines for acceptable quality. Top Pain Points in this segment are Value for Money (15.6%), Bass Performance (12.2%), Design & Build Quality (12.0%).

- ₹2,000–₹4,000 (Average Negative Rate: 12.8%): A critical operational shift occurs here. As Active Noise Cancellation (ANC) becomes a standard inclusion, power consumption management fails. This is the only segment where battery life enters the top consumer complaints. Top Pain Points in this segment are Value for Money (16.3%), Battery Backup (14.0%), Design & Build Quality (12.3%).

- ₹4,000-₹10,000 (Average Negative Rate: 19.5%): Premium buyers exhibit significant buyer’s remorse. The data indicates that legacy audio brands are not able to justify high price tags against the actual product experience. Top Pain Points in this segment are Value for Money (23.8%), Bass Performance (18.2%), Design & Build Quality (18.2%).

3. Brand Performance Scorecard

The market is sharply bifurcated regarding consumer acceptance, proving that the universal negative feedback can be mitigated through disciplined product engineering.

3.1 The Benchmarks:

- realme, OnePlus, and CMF: These brands have successfully established a baseline of trust. By delivering on fundamental technical promises and avoiding glaring functional compromises, they maintain significantly higher customer satisfaction metrics compared to the broader market.

3.2 The Underperformers:

- Noise and boAt: The performance of these volume-driven brands aligns with expectations of a low-satisfaction, mass-market approach. Their models frequently suffer from the aforementioned technical and value gaps.

- Sony (The Legacy Vulnerability): Sony emerges as the most surprising underperformer in this dataset. Despite being an audio pioneer, its entry-level and mid-tier offerings are facing consumer dissatisfaction. This indicates a massive expectation vs. reality gap: Indian consumers hold Sony to an exceptionally high standard based on its legacy, and its sub-₹10,000 models are not meeting that benchmark.

Conclusion

While the sub-₹10,000 TWS market continues to see strong sales volumes, it is currently facing challenges in sustaining brand loyalty. Consumers are increasingly finding their expectations unmet by current offerings, particularly concerning bass optimization, ANC battery management, and an over-reliance on brand legacy. Moving forward, the brands that succeed in this space will likely not be those with the most expansive marketing, but rather those that approach the entry and mid-tier segments with thoughtful product engineering, successfully aligning their price points with a reliable and consistent technical experience.